FMCG market in Australia - statistics & facts

With an estimated population of over 27 million, Australia has an extensive consumer base for fast-moving consumer goods (FMCG) companies to tap into. The country’s FMCG market encompasses products ranging from food and beverages to apparel and beauty and personal care items. Various trends continue to shape and alter Australia’s FMCG landscape, including growing demand for sustainably and ethically produced goods, rising health consciousness, the expansion of e-commerce, and artificial intelligence’s influence on business operations and shopping experiences.

Alongside the major supermarkets, Chemist Warehouse and Priceline are popular retail pharmacies for discount supplements, vitamins, and beauty and personal care items. In the electronics segment, JB Hi-Fi is the market leader in the retail of FMCG electronics. Discount and mid-range department stores Kmart, BIG W, and Myer are also formidable contenders for the FMCG market share due to their broad product ranges, from clothing and footwear to cosmetics and toiletries. However, department stores’ once unique proposition has become increasingly challenged by online marketplaces.

Australia’s FMCG landscape

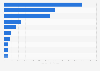

As of June 2024, there were over 156,900 retail trade businesses across Australia, with the country’s retail trade industry revenue exceeding 435 billion Australian dollars that year. Food dominates as the leading retail trade segment, followed by household goods. The country’s food and liquor retail scene has long been dominated by supermarket rivals Woolworths and Coles, with German discount retailer Aldi taking a respectable grocery market share in recent years. When making online grocery purchases, most food purchases remained with the two major domestic supermarkets. With liquor sales largely restricted to licensed liquor stores, both Coles and Woolworths established their own liquor outlets. Coles owns liquor store chain Liquorland, while Woolworths-founded outlets Dan Murphy’s and BWS were spun off from the group in 2021 to form Endeavour Group.Alongside the major supermarkets, Chemist Warehouse and Priceline are popular retail pharmacies for discount supplements, vitamins, and beauty and personal care items. In the electronics segment, JB Hi-Fi is the market leader in the retail of FMCG electronics. Discount and mid-range department stores Kmart, BIG W, and Myer are also formidable contenders for the FMCG market share due to their broad product ranges, from clothing and footwear to cosmetics and toiletries. However, department stores’ once unique proposition has become increasingly challenged by online marketplaces.